By: Steven J Gamboa

With the end of 2021 rapidly approaching, the time has come for year-end tax planning! We’re going to take a look at some tax savings strategies both new and old to help you maximize your deductions and minimize your tax bill for 2021.

Capital Gains Distributions

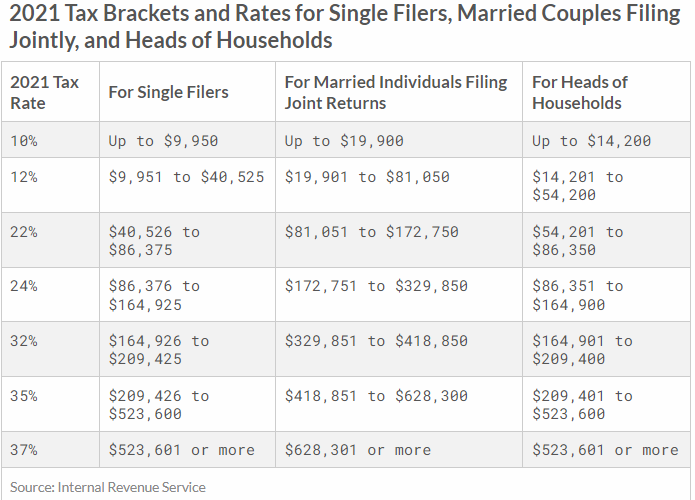

Review your portfolio to see if you have any stocks, bonds, or mutual funds that have declined in value since their initial purchase. Selling them before year-end will create losses to offset any potential capital gains. Remember, long-term capital gains are taxed at 15% if your income is between $40,000 and $445,850, and 20% if higher. Taxpayers are eligible to claim up to $3,000 in capital losses each year, any unused losses in that year are then carried forward to the next year. Short-term capital gains are taxed at the same rate as your ordinary income. Capital gains are netted as follows:

- Short-term losses are netted against short-term gains.

- Long-term losses are netted against long-term gains.

- If either of the preceding two is a net gain while the other is a net loss, they are netted together

Pre-tax Retirement Savings

You can contribute up to $19,500 to a 401(k), 403(b), or federal Thrift Savings Plan in 2021, plus an additional $6,500 in catch-up contributions if you’re 50 or older. These contributions will reduce your take-home pay, therefore reducing your overall tax bill. As these contributions must be made through payroll deductions, the sooner this change is made, the better. It is important to note that if you are contributing to a traditional or Roth IRA for 2021, you have until the tax deadline April 15, 2022, to make those contributions for 2021. And be careful not to go over the contribution limits, as the excess contribution will be both taxable now, and once again when it is eventually withdrawn from the account.

For those who are self-employed with no employees, consider opening up a solo 401(k) plan. You can contribute up to $19,500 (plus an additional $6,500 if you’re 50 or older) to the plan, less any contributions made to an employer’s 401(k) plan for the year. You can also contribute up to 25% of your own net self-employment income to the plan, capping at $58,000 in 2021 ($64,500 if 50 or older). Similarly, a Simplified Employee Pension (SEP) account allows one to contribute 25% of net self-employment income, up to $58,000.

Roth Conversion

It is possible to convert some money from a traditional IRA to a Roth IRA, up to the top end of your income tax bracket. Taxes will be paid on the conversion, but the money will be able to grow tax-free in the Roth account after that. Converting your entire traditional IRA balance can push you into a higher tax bracket but spreading the conversions over several years can be a great tax saving strategy.

Required Minimum Distributions (RMDs)

You must begin making required minimum distributions from your traditional IRA by April 1st of the year after the year you turn 72. Prior to 2020, required minimum distributions began after turning 70 ½ years old. Failing to withdraw RMDs as required could expose you to an excise tax equaling 50% of the excess of the amount you should have withdrawn over the amount actually withdrawn. If you turned 72 in 2021, you make take your first RMD any time before April 1st, 2022. However, this doesn’t necessarily mean to wait until 2022 – if you take your 2021 RMD in 2022, you will still be required to take your 2022 RMD by the end of 2022. This will mean two IRA distributions in the same year, which will be included in your taxable income for a single year. There are situations where this may be beneficial, but it is an important consideration to make. Although you are required to withdraw at least the required minimum distribution amount, you are entitled to withdraw funds exceeding that amount without incurring any penalties. The distributions will be taxed at the same rate RMDs are currently taxed – as ordinary income. All distributions, including the RMD, are reported on Form 1099-R.

Child Tax Credit Changes

The American Rescue Plan, which was enacted in March 2021, introduced major tax law changes including an expansion of the Child Tax Credit for the 2021 tax year. During 2020, the credit was $2,000, was exclusively limited to children 16 years old or younger and was only partially refundable up to $1,400 per child For 2021, the credit is $3,000 per child for children who are between 6 and 17 years old. Additionally, the Child Tax Credit for children who are 5 years old and younger has been increased to $3,600 per child. Additionally, the 2021 credit is fully refundable. The increased credit amounts – $1,000 or $1,600 – begin to phase out and could potentially be reduced to zero for higher income taxpayers. High income taxpayers are classified as joint filers with an AGI of $150,000 or more, head-of-household filers with AGI of $112,500 or more, and all other filers with AGI of $75,000 or more.

Once the increased credit has been reduced, the pre-existing phase out rules utilized in previous years apply to high income taxpayers. This means the remaining credit amount is subject to reduction and could potentially also be reduced to zero for joint filers with an AGI of $400,000 or more and other all other filers with an AGI of $200,000 or more.

Lastly, half of the 2021 Child Tax Credit was paid in advance through monthly payments starting on July 15th and concluding on December 15th. The remaining half will be claimed on your 2021 tax return; therefore, you will need to provide the amounts of the monthly payments received from the IRS during 2021 in order to claim the excess credit on your tax return.

Currently, these expanded provisions only apply to the 2021 tax year, although President Biden plans to extend most of them through 2025 and hopes to make the credit fully refundable on a permanent basis.

Child and Dependent Care Tax Credit

The American Rescue Plan also introduced significant changes to the child and dependent care credit – which again only apply to the 2021 tax year. Child and dependent care expenses include costs incurred for the care of any dependent children under the age of 13 or a qualifying disabled dependent or spouse that lived with you during the year. Major changes included the credit is now fully refundable and the maximum credit percentage has increased from 35% to 50% meaning more care expenses can be used to calculate the allowable credit on your tax return. The maximum allowable child and dependent care credit for the 2021 tax year is $4,000 for one child/disabled person and $8,000 for two or more. Lastly, for 2021 the entire credit will be allowed for taxpayers making less than $125,000. In previous years, the credit-phase-out began once AGI exceeded $15,000.

HSAs

If you are eligible or become eligible to make HSA contributions in December, you can make a full year’s worth of deductible contributions in 2021. The maximum contribution for 2021 is $3,600 for individual coverage, and $7,200 for family coverage. If you are 55 years or older, you can contribute an additional catch-up contribution of $1,000 per year. There are no income limits to be eligible to contribute to an HSA, and withdrawals used for qualified medical expenses are never taxed.

ABLE Accounts

If a family member has special needs, up to $15,000 can be contributed this year to an ABLE account, allowing people with qualifying disabilities to save money without interfering with government benefits. If you are a resident of one of the states that does offer a tax break for these kinds of accounts, your contribution can be deducted. Check out https://www.ablenrc.org/ for further information.

Charitable Deductions

For the 2020 tax year, a new deduction was introduced which allowed for up to $300 of charitable cash contributions to be deducted by taxpayers who claimed the standard deduction. This provision was originally only supposed to apply for 2020 but has now been extended to the 2021 tax year with a slight change. Previously, a $300 deduction per return was allowed, however, for 2021, a $300 deduction per person is allowed meaning married couples can deduct up to $600 of charitable cash contributions if filing a joint 2021 tax return.

Unemployment Compensation

The American Rescue Plan Act made up to $10,200 of unemployment compensation ($20,400 for married couples filing joint) exempt from Federal income tax if their AGI was less than $150,000 during 2020. This exclusion is no longer available which means unemployment compensation earned during the 2021 tax year will once again be taxed entirely.

Annual Gift Exclusion

If you are interested in making a gift of a check and would like it to qualify for the $15,000 annual gift tax exclusion for 2021, there are two requirements that must be satisfied:

- The donee must deposit the check in 2021

- The check must clear in the ordinary course of business (which can happen in January)

A holiday gift of a check that isn’t deposited until after New Year’s is considered a gift in 2022, however a cashier’s check can avoid this problem.

As with all of the above strategies, we highly encourage you to discuss any strategies with your accountant before implementation. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, tax, legal, or accounting advice. You should consult with your own tax, legal, or accounting advisor before engaging in any transaction.