What is a K-1 Tax Form?

A K-1 is used to report a beneficiary’s, partner’s, or shareholder’s share of income, credits, deductions, and more on your personal Income Tax Return. The beneficiary is anyone who has ownership in a business entity. You may be wondering who files a K-1. Luckily, if you are just the beneficiary you only need to report the K-1 rather than prepare the K-1 for the business entity.

Do different business entities issue the same K-1? How do they differ?

Depending on the business entity, they will issue a different K-1. The sections of the K-1’s are similar as you will see, but they have unique features that should be addressed. We will take a look at each K-1 for Partnerships, S-Corporations, and Estates and Trusts and go over the items you may see.

What do you do with a K-1?

When filing your personal taxes, you must be aware if you receive a K-1. If you are being issued a K-1 you must report it. When business entities issue K-1’s to their shareholders or beneficiaries, they first report it to the proper tax authorities like the IRS.

Schedule K-1 for Partnerships

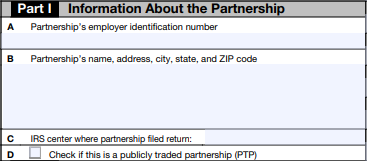

Part I, Information About the Partnership

Part 1 of the K-1 reports on the Information of the Partnership. As you can see from the graphic above you would need your nine-digit Employer Identification Number. This would be required for you to file. After that, you would need the Partnership’s name, address, city, state, and ZIP code. Then the IRS center where the partnership filed the return. Finally, line D has a check box which verifies if this entity is a publicly traded partnership. This is important for your individual tax return. If the entity is a publicly traded partnership, the passive limitations will be applied separately to that activity. Passive limitations are typically applied to the extent of the passive income on the return. Losses not allowed are suspended for this the current tax year and carried over indefinitely. Publicly traded partnerships are not reported on form 8582 as other entities are.

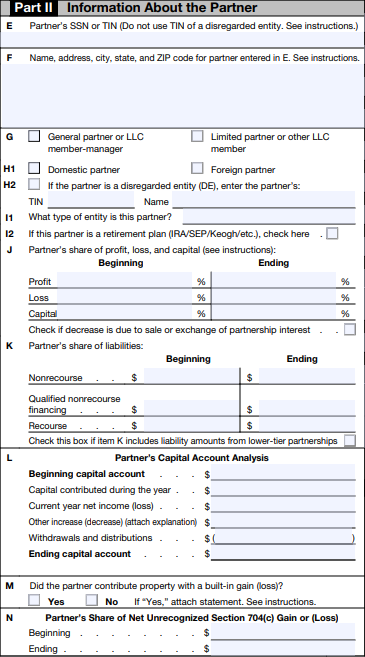

Part II, Information About the Partner

Part 2 of schedule K-1 will show information about the partner receiving the K-1. Similar to the Entity, for items E and F you will need to report the partner’s name, address, state, ZIP code. Once you reach item G you will need to be certain about the facts regarding your situation. Item G outlines the type of partner that this K-1 is being issued to.

The General partner or LLC member-manager indicates that the partner is personally liable for partnership debts. The LLC member-manager is a third-party manager of the LLC. The LLC member-manager is not considered a partner, but a managing member of the company.

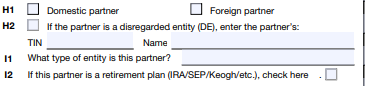

Items H1 through I2 will determine what kind of entity the partner is. Item H1, simply determines whether the partner is operating domestically in the U.S. or in a foreign country outside the U.S. Item H2 and I1 is necessary if the partner is a disregarded entity. A disregarded entity is a term for a business that is separate from the owner but is ignored by the IRS for Federal tax purposes. If so, you would need to provide the Taxpayer Identification Number, and the type of entity. Item I2 determines if the partner is a retirement plan. Partners can make contributions to their retirement plan through the partnership. The contribution amounts are determined by the partner’s net earned income. As we will discuss in part III of the Schedule K-1, the partner’s net earned income is the partner’s earned income less plan contributions and self-employment taxes.

Item K focuses on the partner’s share of liabilities. A Partnerships liability is a recourse liability if any of the partners have a risk of economic loss. Similarly, if the partner has no risk of economic loss, the liability is classified as nonrecourse. Qualified nonrecourse financing includes financing for which the partners are not personally liable for repayment. This financing is only for use in an activity and is loaned out by a qualified person. These qualified persons lending the money can be the federal, state, or local government, as well as anyone in the business of lending. These loans can be anything securable by collateral.

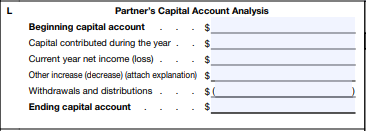

Item L reports the partner’s capital account analysis. This computation is done by calculating the amount of capital the partner contributed to the partnership during the year, as well as your current year net income or loss, withdrawals and distributions made to you, and finally other increases or decreases.

Item M deals with any property the partner may have contributed to the partnership that had a built-in gain or loss. If this is the case the yes box must be checked off a statement should be attached referencing what property was contributed. The statement should include built in gain or loss which is calculated by taking the difference between the Fair Market Value and the partner’s adjusted basis in the property at the time it was contributed.

Item N reports on your share of unrecognized section 704(c) gain or loss. You may receive this for a few reasons:

- You contributed property with the Fair Market Value in excess or less of the adjusted tax basis.

- The partnership elected to revalue the property to reflect changes of the Fair Market Value of the property.

Part III, Partner’s Share of Current Year Income

Partnership reports a wide variety of income sources on their K-1. Luckily, we can look at them in groups.

Box 1 will reflect your share of Ordinary Income from the activities of the partnership. The type of Ordinary income received may change depending on whether you were materially participating in the Partnership’s activities or not.

Box 2 will reflect your share of net Rental Income. This will include your share of income from any rental real estate activities in your possession. This income will typically be reported as a passive activity, but there are some situations that may require that income to be designated as nonpassive income. There are two qualifiers that must be fulfilled to report the income as nonpassive. The first, like box 1, is your material participation. The second is whether you were a real estate professional. Fulfilling both of those qualifications will make all the income in box 2 nonpassive.

Box 3 is similar to box 2, it reports:

The next three items in box 4, will be your share of guaranteed payments. Box 4a is your share of guaranteed payments that the partnership paid you. These payments are not determined by the share of income you may have received. Typically, these payments are listed as nonpassive. Box 4b is for guaranteed payments made for anything not classified as services. Box 4c simply is the total amount guaranteed payments that the partnership made to you, in both 4a and 4b.

The next boxes we look at are your portfolio income. Portfolio income is income that is not generated by the normal activities of the partnership.

Box 5 is your share of interest income. The interest income will be the same as if you received interest income from a from 1099-INT. Partnerships will have to note whether your share of interest income includes interest from credits of clean renewable energy bonds.

Box 6a through 6c are your share of dividends and dividend equivalents. Box 6a is your share of dividends. Like interest it would be the same if you received the dividends from 1099-DIV. Box 6b are your share of qualified dividends. Box 6c are your share of dividend equivalents.

Box 7 is your share of royalty income. Royalty income is any intangible income your partnership generated.

Boxes 8 and 9a are your share of net short-term or net long-term capital gain or loss. These capital gains would also be reported on your Schedule D if you had any other capital gains. Box 9b is your share of 28% rate collectible gains. Collectible gains or losses from the sale or exchange of one of your long-term assets.

Box 9c is your unrecaptured section 1250 gains. Unrecaptured gains can be received in a few different ways. Firstly, you can receive:

Box 10 reports on your net section 1231 gain. This box will be filled if you have any rental activities.

Box 11 Reports on your other income received. You can receive a wide variety of different types of other income. On these boxes you will be seeing an alphabetical letter in the left most box and a numerical value in the right most box, as seen below:

The left most box will determine the classification of your other income, which we will look at later. On the right side of the box is the value associated with the classification. All issued K-1’s follows the same rubric when classifying items on the K-1. Box 11 other incomes classifications are:

- A – Other Portfolio Income(loss)

- B – Involuntary Conversions

- C – Section 1256 Contracts and Straddles

- D – Mining Exploration Costs Recapture

- E – Cancellation of Debt

- F – Section 743(b) Positive Income Adjustments

- G – Reserved for future use

- H – Section 951(a) Income Inclusions

- I – Sections Other Income (Loss)

Part III, Partner’s Share Deductions and Credits

Box 12 is your section 179 Deduction.

Box 13 shows your share of other deductions. Like box 13, this box has codes classifying different items. The classifications for codes A through G determine the type of contributions given:

- A – Cash Contributions (60%)

- B – Cash Contributions (30%)

- C – Noncash Contributions (50%)

- D – Noncash Contributions (30%)

- E – Capital Gain Property to a 50% Organization (30%)

- F – Capital Gain Property (20%)

- G – Contributions (100%)

The Next codes are as follows:

- H – Investment Interest Expense

- I – Deductions – Royalty Income

- J – Section 59(e) Expenditures

- K – Excess Business Interest Expense

- L – Deductions – Portfolio Income (Other)

- M – Amounts paid for medical insurance

- N – Educational Assistance Benefits

- O – Dependent Care Benefits

- P – Preproductive Period Expense

- Q – Reserved for Future Use

- R – Pensions and IRA’s

- S – Reforestation Expense Deduction

- T through U – Reserved for Future Use

- Code V Section 743(b) negative income adjustments

- Code W other deductions

- Code X Reserved for future use

Box 14 is your share of Self-Employment Earnings(loss). Like the prior box, it also had codes classifying each value as follows:

- A – Net Earnings (Loss) from self-employment

- B – Gross farming or fishing income

- C – Gross nonfarm income

Box 15 is your share of credits. These credits may have passive activity limitations if they are passive credits. The classifying codes are as follows:

- A & B – Reserved for Future Use

- C & D – Low-Income Housing Credit

- C – if section 42(j)(5) does apply

- D – if section 42(j)(5) does not apply

- E – Qualified rehabilitation expenditures related to rental real estate

- F – Other rental estate credits

- G – Other rental credits

- H – Undistributed capital gains credits

- I – Biofuel producer credit

- J – Work opportunity credit

- K – Disabled access credit

- L – Empowerment zone employment credit

- M – Increased research activity

- N – Employer Social Security and Medicare Taxes

- O – Backup Withholding

- P – Other Credits

- Theses credits will also be reported on Form 3800

Box 16 determines if you have a Schedule K-3 attached to the K-1. Schedule K-3’s report on your share of International Transactions.

Box 17 Other information

Box 18 activity at risk

Box 19 more than one activity for passive purpose

Box 17 is your share of Alternative Minimum Tax or AMT. The classification codes are as follows:

- A – Post 1986 depreciation adjustments

- B – Adjusted gain or loss

- C – Depletion (other than oil or gas)

- D & E – Oil, gas, & geothermal properties – gross income and deductions

- D – gross income for the above items

- E – Deductions for the above items

- F – Other AMT items

Box 18 is your share of tax-exempt income and nondeductible expenses. The classification codes are as follows:

- A – Tax-exempt Interest Income

- This amount should increase your adjusted basis for the partnership and be reported on your Form 1040 if you are an individual partner

- B – Other tax-exempt income

- Similar to code A the amount should increase your adjusted basis for the partnership, but it will not be reported on your Form 1040

- C – Nondeductible expenses

- These are expenses not deductible on your tax return. This amount will decrease your adjusted basis of your interest in the partnership.

Box 19 is your share of distributions. The classification codes are as follows:

- A – Cash and marketable securities.

- These are the distributions the partnership paid out to you.

- B – Distribution subject to section 737

- C – Other Property

- This item shows the adjusted basis of noncash property before it was distributed to you.

Part III, Partner’s Share of Other Items

Box 20 is your share of other items. The classification codes are as follows:

- A – Investment Income

- B – Investment Expenses

- C – Fuel Tax Credit Information

- D – Qualified rehabilitation expenditures

- E – basis of energy property

- F & G – Recapture of low-income housing credit

- H – Recapture of investment credit

- I – Recapture of other credits

- J – Look-back interest – completed long-term contracts

- K – Look-back interest – income forecast method

- L Dispositions of property with section 179 deductions

- M – Recapture of section 179 deduction

- N – Business interest expense

- This amount should have already been reported as a deduction and is noted for information purposes only.

- O – Section 453(l)(3) information

- P – Section 453A(c) information

- Q – Section 1260(b) information

- R – Interest allocable to production expenditures

- S – Capital construction fund nonqualified withdrawals

- T – Depletion information – oil and gas

- U – Section 743(b) basis adjustment

- V – Unrelated business taxable income

- W – Precontribution gain(loss)

- X- Reserved for use

- Y – Net investment income

- Z – Section 199A information

- AA – Section 704(c) information

- AB – Section 751 gain(loss)

- AC – Section 1(h)(5) gain(loss)

- AD – Deemed section 1250 unrecaptured gain

- AE – Excess taxable income

- AF – Excess business interest income

- AG – Gross receipts for sections 448(c)

- AH – Other information

Box 21 Foreign taxes paid or accrued. These items reduce your partner basis. Something to keep in mind is that this value will not be reported on your Form 1116. It will instead be reported on your Schedule K-3 that we mentioned earlier.

Box 22 allows you to verify if more than one activity is for at-risk purposes.

Box 23 allows you to verify if more than one activity is for passive activity purposes.

Schedule K-1 for S-Corporations

Part I, Information About the Corporation

Part 1 reports on the Information of the Corporation. Again, you will need the nine-digit Employer Identification Number, as well as the Corporation’s name and address.

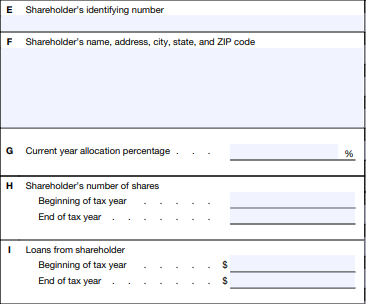

Part II, Information About the Shareholder

Part II reports are more information about the shareholder and their ownership. Item E and F requires the Shareholder’s Social Security Number or Employer Identification Number. Item G has the shareholders current year allocation percentage. Item H shows the number of shares the shareholder owned. Both the beginning number of shares and ending number of shares would be reported. Similar to item I, item H shows the value of loans owned by the shareholder for both the beginning and ending of the tax year.

Part III, Shareholder’s Share of Current Year Income

Box 1 is your share of ordinary business income(loss). Depending on whether the ordinary business income is derived from a passive activity or not it will affect where the income is reported.

Box 2 is your share of Net Rental Real Estate Income(loss). This income is typically from a passive activity. If you are a real estate professional, then this income will be nonpassive.

Box 3 is your share of other net rental income(loss). The amount in this item is passive for all shareholders.

Box 4 is your share of Interest income.

Box 5a is our share of ordinary dividends. Box 5b is your share of Qualified dividends

Box 6 is your share of Royalties

Box 7 is your share of net short-term capital gain(loss)

Box 8a is your share of Net Long-term Capital Gain(loss)

Box 8b is your share of Collectibles (28%) Gain(loss)

Box 8c is your Unrecaptured Section 1250 Gain

Box 9 Net Section 1231 Gain(loss)

Box 10 is your share of other income(loss). This box has codes which classify the items. The codes are the following:

- A – Other portfolio income (loss)

- B – Involuntary Conversions

- C – Section 1256 contracts and straddles

- D – Mining exploration costs recapture

- E – Section 951A(a) income inclusions

- F – Inclusions of subpart F income

- G – Section 951(a)(a)(B) inclusions

- H – Other income (loss)

- The other income in this box have not been included in any of the other items regarding in income or gains and losses.

Part III, Shareholder’s Share of Deductions and Credits

Box 11 is your share of Section 179 deduction

Box 12 is your share of other deductions. The following are its associated classification codes:

- A – Cash contributions (60%)

- B – Cash contributions (30%)

- C – Noncash contributions (50%)

- D – Noncash contributions (30%)

- E – Capital gain property to a 50% limit organization (30%)

- F – Capital gain property (20%)

- G – Contributions (100%)

- H – Investment interest expense

- I – Deductions – Royalty income

- J – Section 59(e)(2) expenditures

- K – reserved for future use

- L – Deductions – Portfolio (other)

- M – Preproductive period expenses

- N – Reserved for future use

- O – Reforestation expense deduction

- P through R – All reserved for future use

- S – Other deductions

Box 13 your share of credits. These credits are your general business credits that can also be seen on form 3800. If your business was a passive activity, then these credits may have passive limitations. The following are its associated classification codes:

- A & B – Reserved for future use

- C & D – Low-income housing credit

- E – Qualified rehabilitation expenditures (rental real estate)

- F – other rental real estate credits

- G – Other rental credits

- H – Undistributed capital gains credit

- I – Biofuel producer credit

- J – Work opportunity credit

- K – Disabled access credit

- L – Empowerment zone employment credit

- M – Credit for increasing research activities

- N – Credit for employer social security and Medicare taxes

- O – Backup withholding

- P – Other Credits

- The credits reported under this code will be further identified in an attached statement. Most credits reported under this code are reported on Form 3800.

Box 14, similar to the other forms determines if you have a Schedule K-3 attached to the K-1. Schedule K-3’s report on your share of International Transactions.

The information going forward is identical across all 3 K-1’s except the labeling of the boxes.

Box 15 is your share of Alternative Minimum Tax or AMT. The classification codes are as follows:

- A – Post 1986 depreciation adjustments

- B – Adjusted gain or loss

- C – Depletion (other than oil or gas)

- D & E – Oil, gas, & geothermal properties – gross income and deductions

- D – gross income for the above items

- E – Deductions for the above items

- F – Other AMT items

Part III, Shareholder’s Share of Other Items

Box 16 shows you any information that would affect your shareholder’s basis.

Box 17 Other information

Box 18 More than one activity for at-risk purposes

Box 19 More than one activity for passive purposes

Schedule K-1 for Estates or Trusts

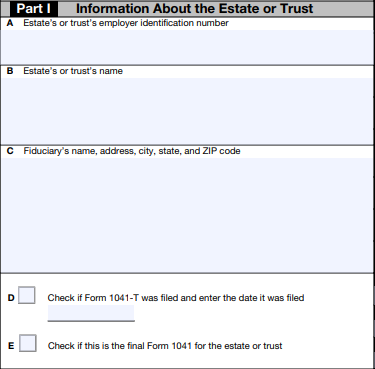

Part I, Information About the Estate or Trust

Item A has the issuing estates or trust ‘s employer identification number. Item B has the Estate’s or trust’s name. Item C has the Estate or trust’s name and address. Item D verifies the date when the K-1 was filed. Item E checks if this is the final K-1 issued after the entity has been disposed.

Part II, Information About the Beneficiary

Part 2 has 3 items. Item F has the beneficiaries ID number which could be a social security number or an employer identification number. Likewise, item G has the name and address associated with the beneficiary. Item H will determine whether the estate or trust is operating domestically or if it is foreign.

Part III, Beneficiary’s Share of Current Year Net Income

These first 3 boxes show your share of taxable interest income, ordinary and qualified dividends.

Box 3 and 4a show your share of short and long-term gain. If the gains are from a passive activity, they will have a statement attached to the K-1.

Box 4b is your share of 28% rate gain. Box 4c is your share of Unrecaptured section 1250 gain.

Box 5 is your share of other portfolio and nonbusiness income. This box contains your share of royalties, annuities, and other income that is not limited to passive limitations. None of the information on this box will be included in any of the other boxes.

These next 3 boxes are your share of business and rental income.

Part III, Beneficiary’s Share of Deductions and Credits

Box 9 is your share of Directly apportioned deductions. This box also has an attached statement which shows all of your directly apportioned deductions.

Box 10 is your share of Estate tax deduction. This amount can be claimed and deducted on Schedule A.

Box 11 is your share of final year deductions. There are different codes that you may see when approaching this item. The following codes are as follows:

- A – Excess Deductions on Termination – Section 67(e)

- B – Excess Deductions on Termination – Non-Miscellaneous Itemized Deductions

- C & D – Unused capital loss carryover

- E & F – Net Operating Loss carryover

- The amounts under this code are the unused net operating loss from terminated trust or decedents. For regular tax purpose code E would be used. For Alternative Tax NOL purposes, code F would apply.

Box 12 is your Alternate minimum tax adjustment. Like box 11, there are also codes associated with the amounts in this box. The codes are the following:

- A – Adjustments for minimum tax purposes

- B – AMT adjustment attributable to qualified dividends

- C – AMT adjustment attributable to net short-term capital gain

- D – AMT adjustment attributable to net long-term capital gain

- E – AMT adjustment attributable to unrecaptured 1250 gain

- F – AMT adjustment attributable to 28% rate gain

- G – Accelerated depreciation

- H – Depletion

- I – Amortization

- J – Exclusion items

Box 13 is your share of credits and credit recapture. There are also codes associated with the amounts in this box. The codes are the following:

- A – Credit for estimated taxes

- B – Credit for backup withholding

- C – low-income housing credit

- D – Rehabilitation credit and energy credit

- E – Other qualifying investment credit

- F – Work opportunity credit

- G – Credit for small employer health insurance premiums

- H – Biofuel producer credit

- I – Credit for increasing research activities

- J – Renewable electricity, refined coal, and Indian coal production credit

- K – Empowerment zone employment credit

- L – Indian employment credit

- M – Orphan drug credit

- N – Credit for employer-provided childcare and facilities

- O – Biodiesel and renewable diesel fuels credit

- P – Credit for employer differential wage payments

- Q – Credit for employer differential wage payments

- R – Recapture of credits

- Z – Other credits

Part III, Beneficiary’s Share of Other Items

Box 14 is your share of other information. This information has codes associated with the amounts as well: The codes are the following:

- A – Tax-exempt interest

- B – Foreign taxes

- C – Reserved for future use

- D – Reserved for future use

- E – Net investment income

- F – Gross farm and fishing income

- G – Foreign trading gross receipts

- H – Adjustments for section 1411 net investment income or deductions

- I – Section 199A information

- Z – Other information

Are there State Differences on a Schedule K-1?

When comparing the differences between the federal and state K-1’s, there are a few items to take note of. The state K-1’s checks the share of income(loss) allocable to the specified state. Typically, a state K-1 would have the federal amounts on it for comparison with the state amounts. In the case where your business entity is operating in multiple states you should also receive multiple state K-1’s. For example, if you had a partnership that operated in both New Jersey and Pennsylvania you would need to determine to which state that income is allocated.

Does a Schedule K-1 count as income?

As you may have seen while looking at the items of the K-1’s, more than just income is included on this schedule. A K-1 may count as income, but not always. There are times when a K-1 may be issued just to account for your share of the business losses during the year.

How does a K-1 affect someone’s personal taxes?

When receiving and reporting a K-1 on your own personal taxes, there are a couple things you need to look out for. If you did receive a K-1 then, that would also mean the IRS also received it, so you should report it on your income tax return. As we have seen, K-1’s will have your share of income and deductions that will be reported on your Individual tax return. Your income or loss will be reported on your Schedule 1 and Schedule E.

What is the difference between investing in a K-1 and other traditional Investments?

By now you have an idea about what the different types of K-1s might show you. But what is the difference between investing in a K-1 or investing in traditional investments like stocks, bonds, or real estate?

Traditional investments are typically the preferred investment for taxpayers. A benefit of investing in traditional investments is that they would issue a Form 1099 at a timely manner for tax filings. The risk for these investments is typically lower than what you would have investing in a K-1. Unfortunately, with lower risk you will also receive a lower payout than you could receive with a K-1.

On the other hand, K-1’s offers the risk of the business entity and is able to typically payout more money to the shareholders due to the structure of the business. Unfortunately, this would mean you would be liable for more taxes at the end of the year. Luckily, K-1’s allow shareholders to deduct their share of losses, deductions, and credits. These items can help shareholders offset some of the end-of-year tax liability.

In the big picture, it may be more beneficial for you to invest in a traditional investment if you are new to investments, as it could save you the potential trouble of a complex return.