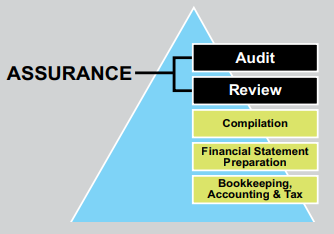

There is some confusion as to the levels of assurance that we can provide in connection an entity’s financial statements. Many people have a misconception that we audit all financial statements that we issue, but there are actually several options that we offer.

If an entity needs a financial statement for management or the owners, we can prepare a financial statement and provide no “assurance” on them. We can do this in connection with bookkeeping services or as a stand-alone engagement. Typically, when we prepare financial statements, we do not include disclosures and often, we do not prepare a full set of financial statements. No formal report is issued on prepared financial statements.

If an entity needs a financial statement for third party users, such as suppliers and lenders, we can issue a compilation report on the financial statements. This can be issued with a full set of disclosures or without. There is a lot of flexibility with a compilation. Also, we do not need to be considered “independent” in order to issue a compilation report. Independence can be impaired when members of our firm or their family members have a financial interest or assume management responsibilities for the entity.

Often, a lender or investor will require limited assurance from us, which is when we recommend reviewed financial statements. A review requires us to be independent and must include a full set of financial statements with all required disclosures. When we perform a review of an entity’s financial statements, we perform analytical procedures, including comparison to budgets, comparisons to historical financial statements, and analysis of financial ratios. We also make inquiries of management. These procedures provide the users of the financial statements with a higher level of assurance.

Finally, there are many times when an audit is required. This includes not-for-profit organizations, required to attach audited financial statements to their state charitable registrations, employee benefit plans required to attach an audit to their annual filing with the U.S. Department of Labor and entities with outside investors or lenders who require a higher level of assurance. An audit includes the requirements for a review, but also requires us to assess fraud and internal control risks and to corroborate the responses to inquiries by management. Procedures used in an audit include confirmation with banks, customers and suppliers, vouching transactions to supporting documentation, and review of subsequent transactions.

At Lear & Pannepacker, we strive to tailor each engagement to the needs of the users, while minimizing the cost. Many times, a lender will agree to a downgrade in the level of assurance required after we advocate for our clients. Give us a call and we can help you better understand your options!